Shareholders may have noticed Jeffries Financial Group, Inc. (NYSE:JEF) filed its first quarter results this time last week. Initial reaction was not positive, with the stock declining 2.7% to $44.10 over the past week. Results were mixed, with earnings per share (EPS) falling short, but revenue exceeding expectations at US$1.7 billion. Statutory profit was US$0.66 per share, 12% below analyst expectations. The analysts have updated their earnings model following these results, but it would be good to know whether they think there's been a big change to the company's outlook, or if it's business as usual. We thought our readers might find interesting the latest (statutory) post-earnings forecasts by the analysts for next year.

Check out our latest analysis for Jefferies Financial Group.

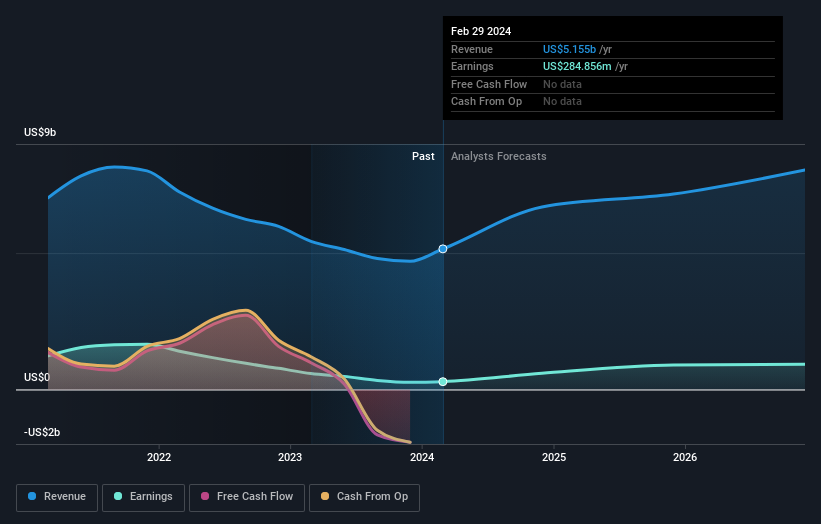

Following the latest results, the 3 analysts covering Jefferies Financial Group have now forecast its revenues in 2024 to be US$6.69b. If achieved, this would reflect a significant 30% improvement in revenue compared to the previous 12 months. Statutory earnings per share are expected to be US$2.67, an increase of 99%. Prior to this report, analysts had modeled 2024 revenue of US$6.35 billion and earnings per share (EPS) of US$3.35. Next year's revenue estimates have increased, but EPS estimates have decreased quite significantly. The consensus suggests a somewhat mixed view of these results.

The consensus price target remains unchanged at US$49.00, suggesting the business is performing roughly in line with expectations, despite some adjustments to earnings and revenue estimates. However, this is not the only conclusion that can be drawn from this data, as some investors like to consider the dispersion of analyst forecasts when assessing price targets. Currently, the most bullish analyst values the Jefferies Financial Group Inc. stock at $52.00 per share, while the most bearish values it at $44.00. A narrow spread of estimates can suggest that the business' prospects are relatively easy to evaluate, or that the analysts have a strong view on its prospects.

While these estimates are interesting, it can be useful to paint a broader picture when comparing Jefferies Financial Group's past performance and forecasts with other companies in its industry. For example, Jefferies Financial Group's growth rate is expected to accelerate significantly, with revenue on an annualized basis projected to show 42% growth by the end of 2024. This is significantly higher than the historic decline of 18% per year over the past three years. Comparing this to analyst forecasts for the industry as a whole, industry revenue is expected to grow by 6.8% per year (in aggregate). As such, Jefferies Financial Group appears to be expected to grow faster than its competitors, at least for some time.

conclusion

Most importantly, the analysts have revised down their earnings per share estimates, indicating a clear drop in sentiment following this result. Pleasingly, they've also upgraded their revenue estimates, with their forecasts suggesting the business is expected to grow faster than the broader industry. The consensus price target is stable at US$49.00, and the latest forecast is not significant enough to impact the price target.

That said, the long-term trajectory of the company's earnings is far more important than next year. Simply Wall St has all of his analyst forecasts for Jefferies Financial His Group out to 2026, available for free on our platform here.

Still, take note of what Jeffries Financial Group shows. 2 warning signs in investment analysis One of them doesn't suit us very well…

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and the articles are not intended as financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.