stock's recent performance driven by its attractive financial outlook?")

Most readers will already know that the Eastern & Oriental Berhad (KLSE:E&O) share price has increased by a hefty 74% over the past three months. Considering the company's impressive performance, we decided to take a closer look at its financial metrics, as a company's financial health over the long term usually drives market results. In this article, we have decided to focus on his ROE for Eastern & Oriental Berhad.

Return on equity or ROE is an important factor to be considered by a shareholder as it indicates how effectively their capital is being reinvested. In other words, this reveals that the company has been successful in turning shareholder investments into profits.

Check out our latest analysis on Oriental and Oriental Berhad.

How do you calculate return on equity?

ROE can be calculated using the following formula:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, Eastern & Oriental Berhad's ROE is:

5.6% = RM120m ÷ RM2.1b (Based on trailing 12 months to December 2023).

“Return” refers to a company's earnings over the past year. This means that for every RM1 of a shareholder's investment, the company will generate a profit of RM0.06 for him.

What is the relationship between ROE and profit growth?

So far, we have learned that ROE is a measure of a company's profitability. Depending on how much of these profits a company reinvests or “retains”, and how effectively it does so, we are then able to assess a company's earnings growth potential. All else being equal, companies with higher return on equity and profit retention typically have higher growth rates compared to companies that don't have the same characteristics.

Eastern & Oriental Berhad's Revenue Growth and ROE 5.6%

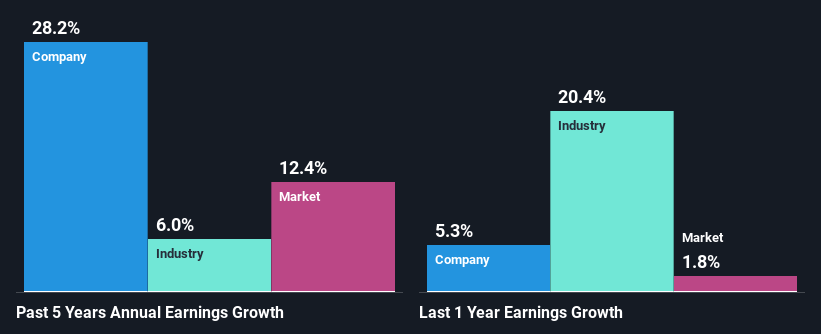

At first glance, Eastern & Oriental Berhad's ROE does not look very attractive. However, upon closer inspection, his ROE for the company is higher than the industry average of his 4.1%, which is hard to miss. Especially considering Eastern & Oriental Berhad's exceptional 28% growth in net profit over the past five years. Note that the company's ROE is moderately low. It's just that the industry's ROE is low. Therefore, there may be other reasons for the increase in revenue. Companies with high earnings retention rates or in high-growth industries.

We then compare it to the industry's net income growth rate, which is great to see that Eastern & Oriental Berhad's growth rate is quite high when compared to the industry average growth rate of 6.0% over the same period.

Earnings growth is an important metric to consider when evaluating a stock. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). Doing so will help you determine whether a stock's future is promising or ominous. One good indicator of expected earnings growth is the P/E ratio, which determines the price the market is willing to pay for a stock based on its earnings outlook. So you might want to check whether Eastern & Oriental Berhad is trading on a higher or lower P/E relative to its industry.

Does Eastern & Oriental Berhad reinvest its profits efficiently?

Eastern & Oriental Berhad does not pay dividends to its shareholders. This means that the company reinvests all of its profits back into the business. This is likely what is driving the high earnings growth rate discussed above.

summary

Overall, I feel that Eastern & Oriental Berhad's performance was very good. In particular, it's great to see that the company is seeing strong earnings growth, backed by an excellent ROE and high reinvestment rate. If the company continues to grow its revenue as it has, it could have a positive impact on the stock price, given how earnings per share affect the stock price over the long term. Don't forget that business risk is also one of the factors that affect stock prices. Therefore, this is also an important area that investors need to pay attention to before making decisions about the business. To learn about the four risks he has identified for Eastern and Oriental Berhad, visit our risks dashboard for free.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.