stock indicate that the market may be wrong given its solid financial outlook?")

It's hard to get excited about Allgaier's (ETR:AEIN) recent performance, with its share price down 7.8% over the past month. But if you pay close attention, given how the market typically rewards companies with strong financial health, the company's strong financials could mean a higher share price over the long term. You may be wondering if that means something. In this article, we decided to focus on Allgaier's ROE.

Return on equity or ROE is a key measure used to evaluate how efficiently a company's management is utilizing the company's capital. In other words, this reveals that the company has been successful in turning shareholder investments into profits.

Check out our latest analysis for Allgaier.

How is ROE calculated?

of Calculation formula for return on equity teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, the ROE for Allgayer is:

9.0% = €17 million ÷ €189 million (based on the trailing twelve months to December 2023).

“Earnings” is the amount of your after-tax earnings over the past 12 months. Another way to think of it is that for every 1 euro worth of stock, the company allowed him to earn a profit of 0.09 euros.

What is the relationship between ROE and profit growth rate?

So far, we have learned that ROE measures how efficiently a company is generating its profits. We are then able to assess a company's future ability to generate profits based on how much of its profits it chooses to reinvest or “retain.” Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company's growth rate compared to companies that don't necessarily have these characteristics.

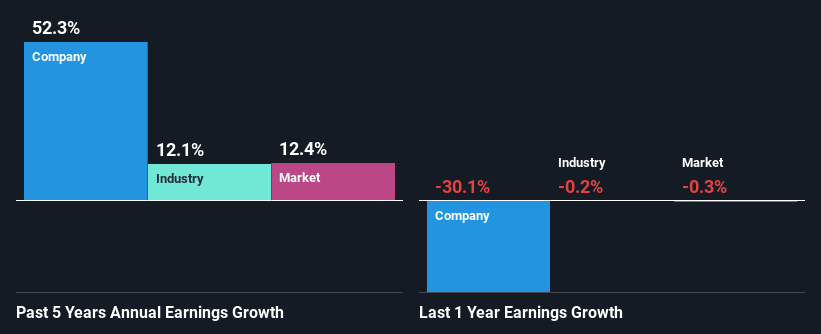

Allgeier's earnings growth and ROE 9.0%

First, Allgaier's ROE looks acceptable. That said, the company's ROE is still significantly lower than the industry average of 13%. If so, his massive 52% increase in net income over five years, reported by Allgeier, is a pleasant surprise. Therefore, there may be other causes behind this growth. Maintaining high profits and efficient management, etc. Keep in mind, the company has a respectable ROE. It's just that the industry's ROE is high. So this certainly also provides a backdrop for the high revenue growth the company is seeing.

Next, if we compare it to the industry's net income growth, we find that Allgeier's growth is quite high when compared to the industry average growth rate of 12% over the same period, which is great.

Earnings growth is a big factor in stock valuation. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). That way, you'll know if the stock is headed for clear blue waters or if a swamp awaits. Is AEIN fairly valued? This infographic about a company's intrinsic value has everything you need to know.

Is Allgeier using its profits efficiently?

Allgeier's median three-year payout ratio is 46% (retaining 54% of its earnings), which is neither too low nor too high. This suggests that the company's dividend is well covered, and given the high growth discussed above, Allgaier appears to be reinvesting its earnings efficiently.

Additionally, Allgaier has been paying dividends for six years. This means that the company is quite serious about sharing profits with shareholders. After researching the latest analyst consensus data, we find that the company's future dividend payout ratio is expected to decline to 27% over the next three years. The company's ROE is expected to rise to 17% over the same period, which can be explained by the lower dividend payout ratio.

conclusion

Overall, we are very satisfied with Algayer's performance. In particular, we like that the company reinvests heavily in its business at a reasonable rate of return. Unsurprisingly, this led to impressive revenue growth. Having said that, a review of the latest analyst forecasts indicates that the company's future revenue growth is expected to slow. To know more about the latest analyst forecasts for the company, check out this visualization of analyst forecasts for the company.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.