Dutch Lady Milk Industries Berhad (KLSE:DLADY) has been performing well on the share market, with its share price up by 38% over the past three months. Since share prices generally move in tandem with a company's financial performance over the long term, we decided to take a closer look at the company's financial indicators to see if they have influenced the recent share price movements. In particular, we'll be looking at Dutch Lady Milk Industries Berhad's ROE today.

Return on Equity (ROE) is a measure of how effectively a company is growing its value and managing investors' money. In other words, it is a profitability ratio that measures the rate of return on the capital provided by a company's shareholders.

Check out our latest analysis for Dutch Lady Milk Industries Berhad

How do you calculate return on equity?

ROE can be calculated using the following formula:

Return on Equity = Net Income (from continuing operations) / Shareholders' Equity

So, based on the above formula, the ROE for Dutch Lady Milk Industries Berhad is:

17% = RM72m ÷ RM437m (Based on the trailing twelve months to December 2023).

“Return” refers to annual profit, meaning that for every MYR1 of shareholder investment, the company generates a profit of MYR0.17.

What is the relationship between ROE and earnings growth?

Thus far, we have learned that ROE is a measure of how efficiently a company is generating its profits. Next, we need to evaluate how much of its profits the company is reinvesting or “retaining” for future growth. This gives us an idea about a company's growth potential. Assuming all other things are equal, companies with both a higher return on equity and retained profits are usually companies with higher growth rates compared to companies that don't share the same characteristics.

Dutch Lady Milk Industries Inc.'s earnings growth and 17% ROE

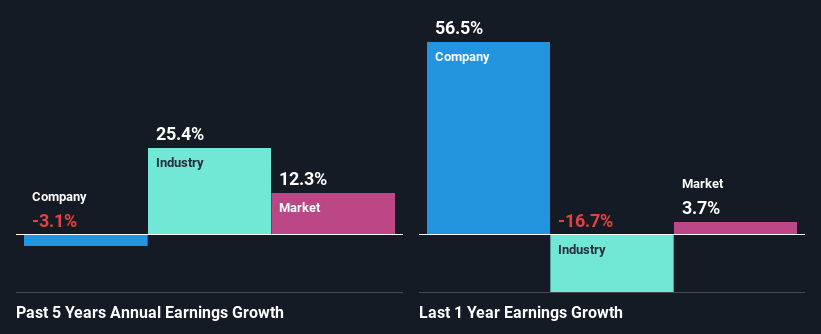

First, Dutch Lady Milk Industries' ROE looks reasonable. Moreover, the company's ROE compares favorably with the industry average of 7.5%. Needless to say, it is surprising to see that Dutch Lady Milk Industries' net income has declined by 3.1% over the past five years. Therefore, there may be other aspects to the reason for this, such as the company's high dividend payout ratio or inadequate capital allocation.

So, the next step is to compare Dutch Lady Milk Industries Berhad's performance with the industry, which is disappointing as it shows that the company's revenue is shrinking, while the industry has increased its revenue by 25% over the past few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is whether the expected earnings growth, or lack thereof, is already priced into the share price. Doing so will help them determine whether the stock's future is promising or ominous. One good indicator of expected earnings growth is the P/E ratio, which determines the price the market is willing to pay for a stock based on its earnings outlook. Therefore, it is a good idea to check whether Dutch Lady Milk Industries Berhad is trading at a high P/E or a low P/E compared to the industry.

Is Dutch Lady Milk Industries Berhad making good use of its profits?

With a high three-year median payout ratio of 57% (43% of profits are retained), most of Dutch Lady Milk Industries' profits are paid out to shareholders, which is why the company's earnings are declining, leaving the company with little capital to reinvest – a vicious cycle that will not benefit the company in the long run.

Moreover, Dutch Lady Milk Industries has been paying dividends for at least 10 years, suggesting that continuing to pay dividends is far more important to management, even at the expense of business growth. Our most recent analyst data indicates that the company's dividend payout ratio is expected to fall to 40% over the next three years.

summary

Overall, we feel that Dutch Lady Milk Industries Berhad certainly has some positive factors to consider. However, we are a bit concerned by the low earnings growth rate, especially given the company's high profitability. Investors could have benefited from a higher ROE if the company had reinvested more of its profits. As mentioned earlier, the company retains a small portion of its profits. That said, looking at current analyst forecasts, the company's earnings growth rate is expected to improve significantly. You can learn more about the company's future earnings growth forecast here. free For more information, see the company's analyst forecast report.

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.