stock?")

Most readers will already know that the VEEM (ASX:VEE) share price has increased by a hefty 57% over the past three months. Considering the company's impressive performance, we decided to take a closer look at its financial metrics, as a company's financial health over the long term usually drives market results. In this article, we decided to focus on VEEM's ROE.

Return on equity or ROE is a key measure used to evaluate how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio that measures the rate of return on the capital provided by a company's shareholders.

Check out our latest analysis for VEEM.

How do you calculate return on equity?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, the ROE for VEEM is:

12% = AUD 5.8 million ÷ AUD 50 million (based on the trailing twelve months to December 2023).

“Return” is the annual profit. This means that for every A$1 of a shareholder's investment, the company will generate a profit of A$0.12 for him.

Why is ROE important for profit growth?

It has already been established that ROE serves as an indicator of how efficiently a company will generate future profits. Now we need to evaluate how much profit the company reinvests or “retains” for future growth, which gives us an idea about the company's growth potential. Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company's growth rate compared to companies that don't necessarily have these characteristics.

VEEM's Revenue Growth and ROE of 12%

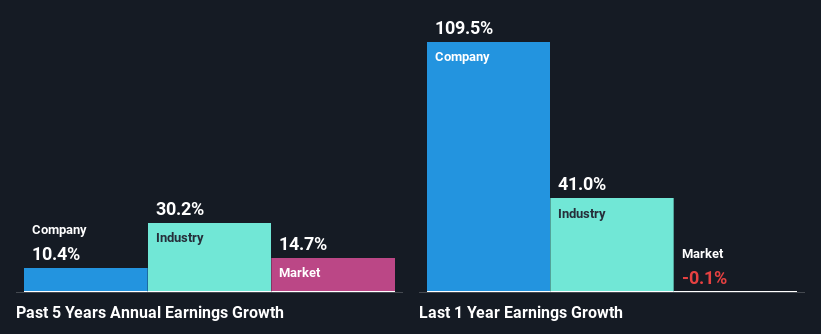

First, VEEM's ROE looks acceptable. Moreover, the company's ROE is in line with the industry average of 13%. As a result, this likely laid the foundation for the decent 10% growth his VEEM has seen over the past five years.

As a next step, we compared VEEM's net income growth to the industry, and were disappointed to find that the company's growth was lower than the industry average growth of 30% over the same period.

The foundations that give a company value have a lot to do with its revenue growth. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). That way, you'll know if the stock is headed for clear blue waters or if a swamp awaits. If you're wondering about VEEM's valuation, check out this gauge of its price-to-earnings ratio compared to its industry.

Is VEEM reinvesting its profits efficiently?

With a median three-year dividend payout ratio of 30% (meaning the company retains 70% of its profits), VEEM has seen considerable growth in its earnings and is well covered. It appears to be reinvesting as efficiently as it is paying dividends. .

Furthermore, VEEM is determined to continue sharing its profits with its shareholders, as can be inferred from its long history of dividend payments over 7 years. Based on our latest analyst data, the company's future payout ratio over the next three years is expected to be around 30%. Therefore, the company's future ROE is not expected to change much, with analysts forecasting it to be 13%.

conclusion

Overall, we feel that VEEM's performance is very good. In particular, it's great to see that the company has invested heavily in its business, delivering strong revenue growth, along with high rates of return. That said, the company's earnings are expected to accelerate, according to the latest industry analyst forecasts. Are these analyst forecasts based on broader expectations for the industry, or are they based on the company's fundamentals? Click here to be taken to our analyst forecasts page for the company .

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.