Regarding quarterly results, Amazon (NASDAQ:AMZN) Shareholders have nothing to complain about for now. The e-commerce giant reported first-quarter sales of $143.3 billion and earnings per share of $0.98, both of which beat expectations and significantly exceeded the year-ago period. Amazon shares rose slightly following the release of the company's first quarter report on Tuesday night. Get more wins for obvious reasons.

However, there are some less obvious reasons to buy Amazon stock, which further strengthen our already bullish view.

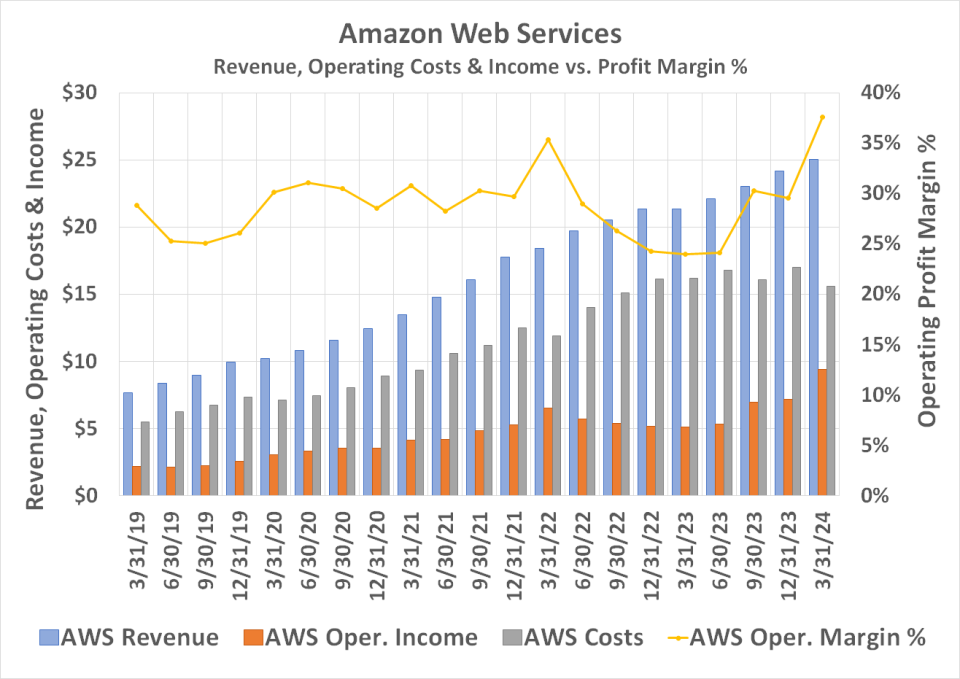

1. Amazon Web Services is now much more cost-effective.

Perhaps one of Amazon's most exciting growth engines at the moment is its cloud computing division. In fact, Amazon Web Services (AWS) has been growing at a double-digit pace for several years. However, the business hit an alarming wall from mid-2022, thanks to the huge costs of running a cloud computing sector in an inflation-ridden environment. Despite AWS's cloud revenue continuing to grow, its operating profit and operating margin have been stagnant since 2022.

However, this situation appears to have changed dramatically in the last quarter. Following a slight turnaround that began to take shape in the third quarter of last year, AWS operating margins rose to a record-breaking 37.6% in the first quarter of this year.

Deliberate cost containment certainly helped. The benefit is that inflation is at least starting to level out. Then there are economies of scale. In other words, the bigger your business, the more cost-effectively you can manage it.

Whatever the reason, these margin expansions are a sizeable and encouraging deal, considering Amazon Web Services accounts for nearly two-thirds of Amazon's operating profits.

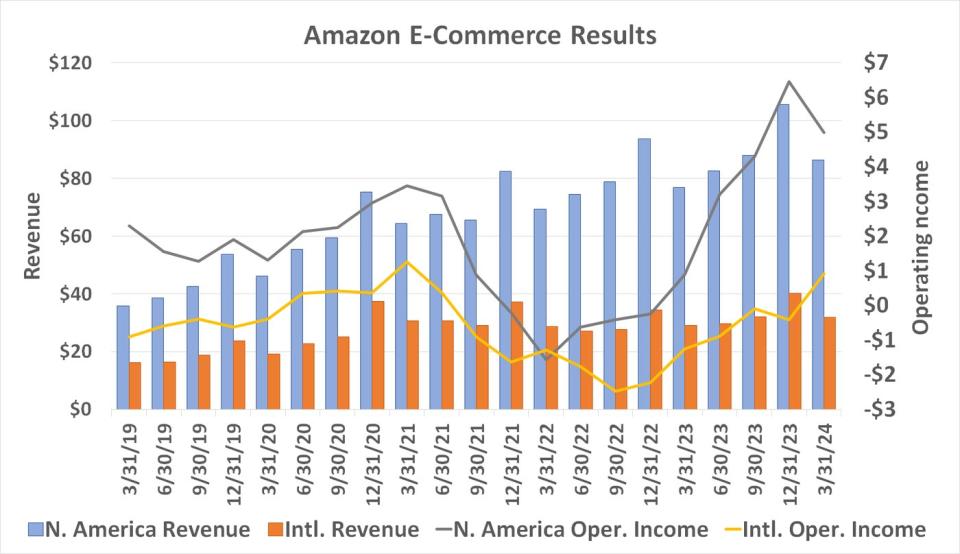

2. E-commerce is (finally) a business worth running

That's interesting. In its early days, Amazon was far more concerned with expanding its reach than making profits. And investors OKed the idea. But the company showed no interest in further accelerating its profit growth. Even when it probably could have been. Shareholders have become so accustomed to low profit margins that they no longer pursue the issue seriously.

Now, surprisingly (and without much fanfare), Amazon's e-commerce business is finally making a surprisingly wide range of profits. Following a record fourth quarter operating profit, first quarter e-commerce operating profit of $5.9 billion marks a new record for the calendar quarter. This is impressive considering how problematic inflation is for both businesses and consumers.

But perhaps the most compelling data provided in the graph above is that Amazon's international e-commerce business has This means that the company is back in the black. This will help justify the company's continued investment in its overseas operations, where the bulk of its future growth is expected to be. The North American market is quite saturated.

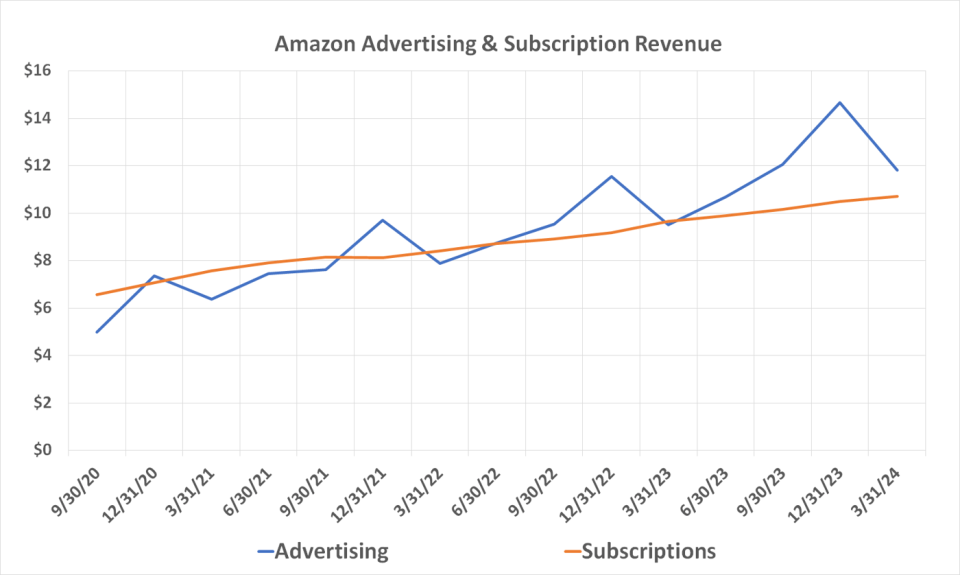

3. Advertising and subscription revenue skyrockets

But why has Amazon's e-commerce business suddenly become so profitable? Increased scale and increased efficiency are certainly factors. But business is also evolving. Amazon.com is becoming more of an advertising platform than just an online mall.

ohFor the record, it was almost always one. That is, a third-party seller has long been able to pay a fee to have his products featured more prominently on his website. But over the past few years, the business has gotten even hotter. Last quarter, advertising revenue was $11.8 billion, an increase of 24% year-over-year, extending an established growth trend. This is also a highly profitable income.

Another dataset shown in the chart above maps the growth of Amazon's subscription business. This is primarily revenue driven by subscriptions to Amazon Prime, but may also include other subscription-based services, such as digital music or grocery delivery. Last quarter, subscription revenue reached a record $10.7 billion, up 11% year-over-year.

This continued growth is no small thing, but it's not necessarily for the reasons you might think. It's not so much about income. These subscribers are known to spend more money on Amazon than non-subscribers. The increase in this number simply indicates that the company is adding more fruitful customers to its active customer count.

All of this makes Amazon stock an even better buy

Of course, these aren't the only reasons to own Amazon stock. The big, obvious ones still remain. These include the company's e-commerce market dominance and continued expansion. Amazon Web Services is also an attractive business, whether or not its margins are improving.

Nevertheless, these details make an already solid bullish argument even better. Amazon leverages its unique strengths, such as its massive size and technological capabilities, to do both big and small things well. Few other companies can match both.

Should you invest $1,000 in Amazon right now?

Before buying stocks on Amazon, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks For investors to buy now…and Amazon wasn't among them. These 10 stocks have the potential to generate impressive returns over the next few years.

when to think about it Nvidia This list was created on April 15, 2005…if you invested $1,000 at the time of recommendation. you have $544,015!*

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor For the service more than 4 times The resurgence of the S&P 500 since 2002*.

See 10 stocks »

*Stock Advisor will return as of April 30, 2024

John Mackey, former CEO of Amazon subsidiary Whole Foods Market, is a member of the Motley Fool's board of directors. James Brumley has no position in any stocks mentioned. The Motley Fool owns a position in and recommends Amazon. The Motley Fool has a disclosure policy.

“3 Surprising Reasons Investors Should Buy Amazon Stock Now” was originally published by The Motley Fool.